[Strategy] Net Zero GHG Emissions in Our Financed Portfolio

Net Zero GHG Emissions in Our Financed Portfolio

2030 Interim Targets

MUFG joined NZBA in June 2021 after announcing the Carbon Neutrality Declaration. NZBA members share a common goal: net zero financed portfolios by 2050. They are also required to set interim targets for 2030 or earlier using a science-based approach.

We are committed to helping achieve the goals of the Paris Agreement by achieving carbon neutrality by 2050, and at the same time, supporting a smooth transition to a decarbonized society through our financial services, and proactively contributing to creating a sustainable society by fostering a virtuous cycle between the environment and the economy. Today, we have set interim targets for 2030, aligned with the Paris Agreement. We recognize that the processes for achieving these targets vary depending on the characteristics of each region and business. We are also aware that our business is greatly affected by geopolitical risks and other factors, so we will share issues that we find through engagement (dialogue) with customers and support them to help resolve these issues.

Innovations which are still in the conceptual stage is another indispensable element for the world to achieve decarbonization. We believe that there is a gap between the real world and the goal that is yet to be materialized. Therefore, our aspiration is to further contribute to the changes where the world advances more towards decarbonization by developing research on new technologies for implementation.

To reflect our stance mentioned above, we have set ranged interim targets in order to work together with our stakeholders to achieve net zero GHG emissions by 2050.

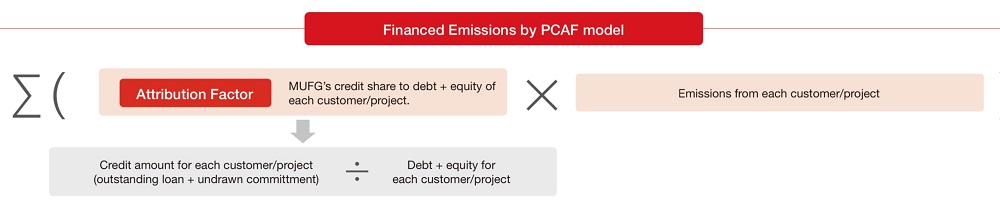

Net zero GHG emissions from the financed portfolio means decarbonizing the sector portfolio by reducing the GHG (Scope3) generated through financing customers and projects.

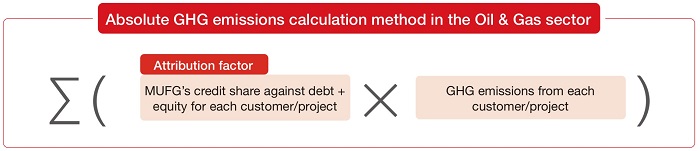

GHG emissions from the financed portfolio are defined as “financed emissions”. This is the amount of GHG emissions attributed to each financial institution through financing each customer or project.

MUFG uses the calculation model recommended by the PCAF. When calculating MUFG’s attribution factor, while the PCAF guidelines recommend using outstanding amounts of loans and investments, MUFG uses outstanding credit amount which includes the undrawn amount of commitment in order to reflect our credit stance as a financial institution more accurately.

Four Approaches to Setting Interim Targets

We have adopted the following four approaches to setting the interim target.

Going forward, we will reflect the changes in the IEA (International Energy Agency) scenario and various guidelines, as well as the increase in the quality of data disclosed by our customers, as appropriate.

■ Science-based

Following the NZBA Guideline, MUFG will ensure that the interim target for 2030 is scientifically “well below 2˚C, preferably to 1.5˚C,” as agreed in the Paris Agreement.

As a benchmark for 1.5°C, we will refer to scientific scenarios published by IEA and others.

■ Data quality

We use the best available data to set targets. However, there are limits to the amount and quality of data currently available, so we will use the PCAF data quality score to check the quality of emissions data disclosed by MUFG.

When data is updated or new data is disclosed, improvements in accuracy and quality will be reflected. MUFG will also contribute to improving data accuracy by being highly transparent when disclosing information.

■ Highly standardized and transparent

MUFG believes that targets should be set from a global perspective using widely accepted and transparent methods. We participate in various initiatives, collecting insights and reflecting them in the targets we set.

We will proceed with target setting, incorporating guidelines and rules developed by NZBA, PCAF, PACTA, and SBTi etc., as well as the outcomes of the global working groups which we participate in.

■ Sector-specific

Pathways and the methods to achieve carbon neutrality vary by sector, so for each sector we will take into consideration the characteristics of the business, the guidelines and the targets set by each customer.

By taking this approach, MUFG will identify issues in each sector and support customers’ efforts for achieving carbon neutrality.

Interim Target-Setting Process

Initiatives by Sector

■ Power sector

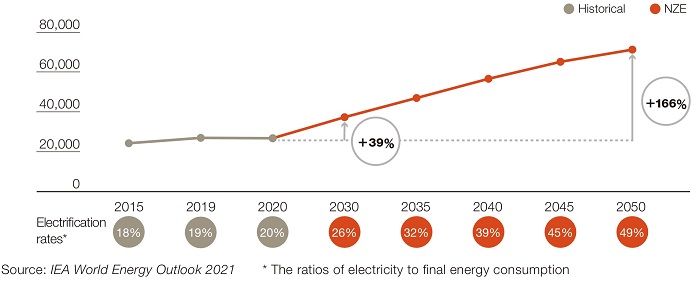

In the transition stage to a decarbonized society, the demand for power is expected to increase due to economic growth in developing countries and the electrification of industry. So, the power sector will need to shift to renewable energy and low-carbon fuels, while ensuring a stable supply of energy(note).

The policies and initiatives of each country are important because the business model of this sector is local and therefore has particularly strong regional characteristics.

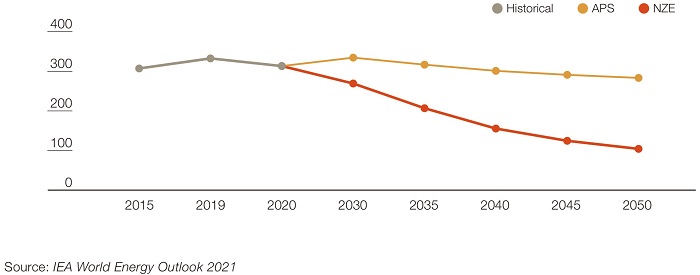

- Electricity demand under the IEA 1.5°C scenario (IEA NZE scenario in which the increase in the global surface temperature rise is limited to 1.5°C with a 50% or greater probability of success) is estimated to grow by 39% by 2030 and 166% by 2050 (compared with 2020).

| Envisioned Business Opportunities | Risk Management |

|---|---|

● Investment in renewable energy (short, medium, long): Capital investment aimed at expanding renewable energy. Approximately four times the renewable energy capacity as of 2021 in Japan and overseas is required to achieve the 1.5°C scenario in 2030.

● Investment in transmission and distribution network (short, medium, long): Technology development and capital investment for flexible power supply through grid enhancement, energy storage systems, etc.

● Investment in innovative technologies (medium, long): Fund raising for R&D, demonstration projects, and practical application of decarbonized thermal power (hydrogen power generation, etc.), next-generation nuclear reactors, next-generation solar power, long duration energy storage technology (LDES), etc.

● Investment in ammonia/hydrogen energy and CCUS (short, medium, long) |

● Reduction of GHGs from financed portfolio Interim target setting, performance management ● Management of transition risks Understanding and confirming transition strategies through engagement ● Reduction of environmental and social risks based on Environmental and Social (ES) policy Prohibition of investment and financing in new and expanded coal-fired power generation ● Setting finance targets for coal-fired power generation |

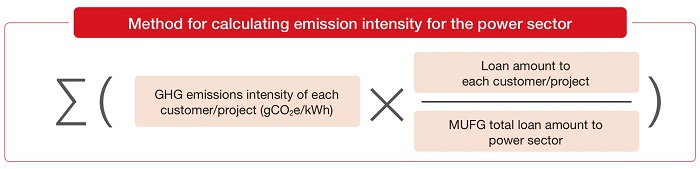

Calculation methodology for emission intensity in the power sector

| Target scope | Value chain: Power generation businesses Emission scope: Scope 1 |

|---|---|

| Asset scope | Loan amounts (including undrawn-committed amounts)(note) (note) More than 85% of the exposure is included in the calculation. |

Target metric |

Emission intensity (gCO2e/kwh) |

| Data source | Information disclosed by each customer, CDP, Bloomberg, etc. |

(Target scope)

Following SBTi and PACTA, the value chain and emission scope which we cover is Scope 1 of the power generation business, which accounts for the majority of GHG emissions in this sector.

(Target metric)

The power sector is expected to take a leading role in driving cross-industry decarbonization. GHG emission intensity, a measure of emission efficiency, will be used as the metric because the power sector needs to support the increasing electricity demand while simultaneously moving ahead with clean energy conversion.

Interim target setting

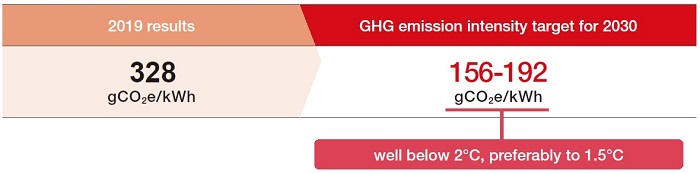

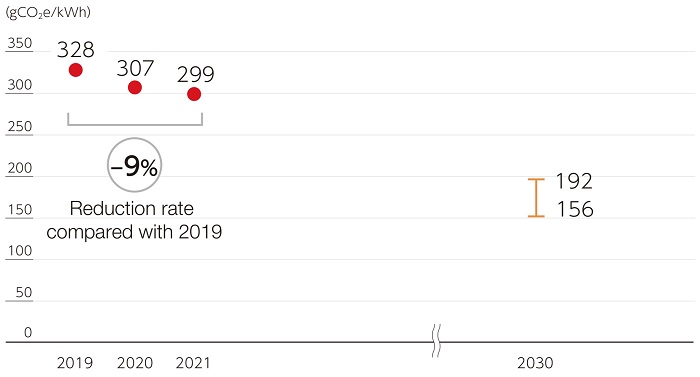

The interim target for 2030 is 156-192gCO2e/kWh.

The power sector has a local business model with strong regional characteristics, and is expected to take a leading role in promoting each NDC(note) with governments. We will achieve 192gCO2e/kWh by supporting our customers to meet each country’s NDCs, which are essential for achieving the Paris Agreement, and also by helping their initiatives for green, transition and innovation. 192gCO2e/ kWh is a level well below the IEA 2˚C scenario in 2030.

In addition to the above, we aim for 156gCO2e/kWh, which is consistent with the IEA 1.5˚C scenario in 2030, by making further contributions to the promotion of renewable energy, etc. as a leading company in sustainable finance.

- Nationally Determined Contribution. This report, submitted by over 190 countries, shows how much each country will contribute to reducing GHGs under the Paris Agreement. An update to the report is required every five years

Results over time

As of March 2022, the emission intensity of the power sector was 299gCO2e/kWh, a decrease of about 9% from 328gCO2e/kWh in the base year of 2019. This is due to the progress in decarbonization of our customers.

MUFG will support our customers’ initiatives for green, transition, and innovation to achieve the 2030 target, and will contribute to the promotion of renewable energy etc. as a leading company in sustainable finance.

| Target for implementation | Outline of initiatives |

|---|---|

| Initiatives toward Japanese companies | In December 2022, we established a new Power Project Team (PT) focused on the power sector, a key sector in achieving carbon neutrality in Japan. The PT is working to strengthen relationships with power utilities and industry associations by holding bi-weekly internal sessions with invited external experts to deepen understanding of related policy trends and complex power system structures. Participating members include head of branches which are in charge of electric power utilities nationwide as well as management from relevant divisions at the bank headquarters. The sessions are aimed at strengthening customer approach through management-level discussions. Activities are aimed at not only reinforcing knowledge but also strengthening cooperation among power sector sales managers, with sales managers from around country gathering to tour customers' nuclear power-related facilities, power plants, and other facilities. |

MUFG continuously coordinates dialogue between customers and overseas institutional investors to aid in eliminating the gap between these parties regarding the recognition of ideals and reality in the achievement of carbon neutrality. Through interviews with overseas investors, we recently shared analyses of the impacts on corporate value of customers' ESG responses, and conducted exchanges of ideas on approaches to respective transition, thereby contributing to the building of a foundation for customers' future strategy formulation. |

|

MUFG conducts in-bank study sessions with invited experts to enhance industry knowledge, and continuously works toward a multi-faceted understanding of customers' external environments and awareness of issues, through means including tours of power generation facilities and regular exchanges of ideas with top management and other parties in customer organizations. Through such activities, we discuss optimal ways by which MUFG can contribute to customers' formulation and implementation of strategies without being bound by conventional frameworks, including the possibility of strategic investment and provision of human capital to achieve the shared goals of customers and MUFG. |

|

| Company A (EMEA) | MUFG leveraged its strong relationship with a listed UK company with renewable electricity generation and electricity network businesses and conducted continuous dialogue with its Treasury and Sustainability teams. Through client engagement, MUFG was appointed as a Sole Sustainability Coordinator in two Sustainability-linked loans – one for transmission and one for distribution - and advised the client based on their unique ESG footprint and strategy for the two business entities. |

| Company B Group (APAC) | Group Company B has set their 2050 net zero goal and has also set mid and long-term GHG emission reduction targets for their key and emerging businesses to meet the group’s net zero ambitions. Through consistent outreach by a combination of MUFG’s front RMs, Product Office, Sector Coverage teams, MUFG engaged the parent holding company and their subsidiaries in power and telecom sectors and established the parent holding company’s debut SLL and green loan for their overseas renewable energy projects. |

| Company C (Americas) | MUFG acted as a lead arranger in JICA PSIF (JICA Private Sector Investment Finance) facility and provided financing towards capex for improvement and development of a power grid in low-income region in Brazil. The financing will support innovative solution for power distribution namely improvements in energy efficiency, increase power distribution capacity and reducing losses. |

Promotion of Renewable Energy Business-Related Financing

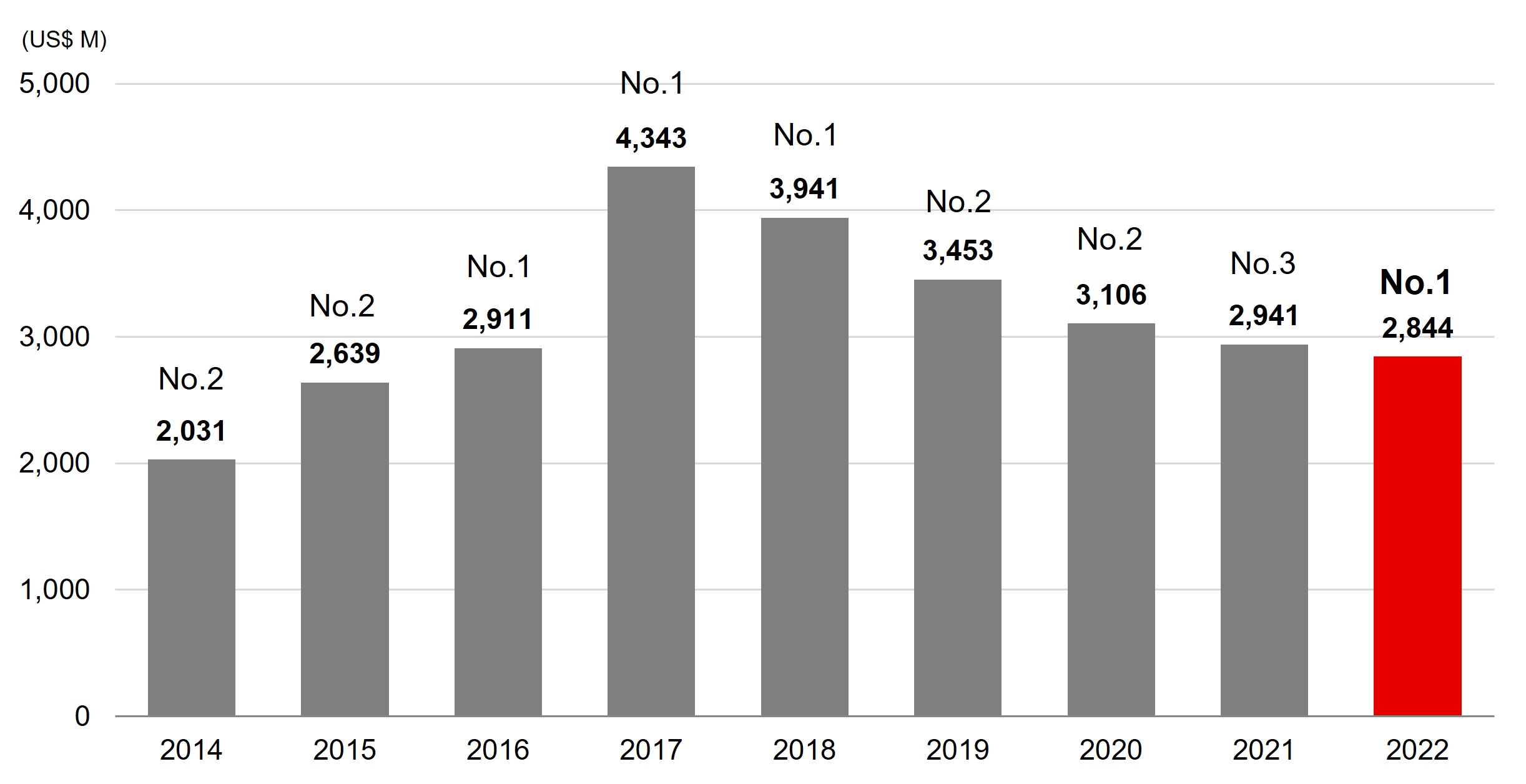

MUFG is one of the world's top performers in the global project finance sector, as shown in the Lead Arrangers League Table related to renewable energy projects.

In May 2021, MUFG set a target of reducing CO2 emissions through project finance for renewable energy projects by a cumulative total of 70 million tons from FY 2019 to FY 2030. This is equivalent to the annual CO2 emissions of about half of the households in Japan.

Through FY2022, we have reduced CO2 emissions by a cumulative 36.63 million tons.

- Source: Bloomberg New Energy Finance ASSET FINANCE / Lead Arrangers LEAGUE TABLE

Initiatives toward Renewable Energy Project Financing

| Country | Target of support | Project overview |

|---|---|---|

Japan |

Offshore wind power generation | MUFG supports all the offshore wind power projects in Japan, including the Akita Offshore Wind project. |

| Japan | Solar power generation | Achieved financial close for the first distributed solar generation project based on Corporate PPA structure in Japan. |

| U.S. | Transmission lines | Project finance for underground and underwater transmission line projects, increasing renewable power transmission capacity in New York metropolitan area. |

| Portugal, Spain | Solar and wind power generation | Refinancing of the largest platform of onshore wind and solar PV in Iberia cementing MUFG’s presence in the region. |

| India | Solar and wind power generation, storage batteries | The first hybrid renewable round-the-clock battery-enabled project in India. Complemented with storage capacity, the project will be able to provide electricity for 24 hours. |

| Australia | Wind power generation | MUFG provides project finance to support the acquisition of operational wind farms with one of the largest renewable energy developers in Australia. |

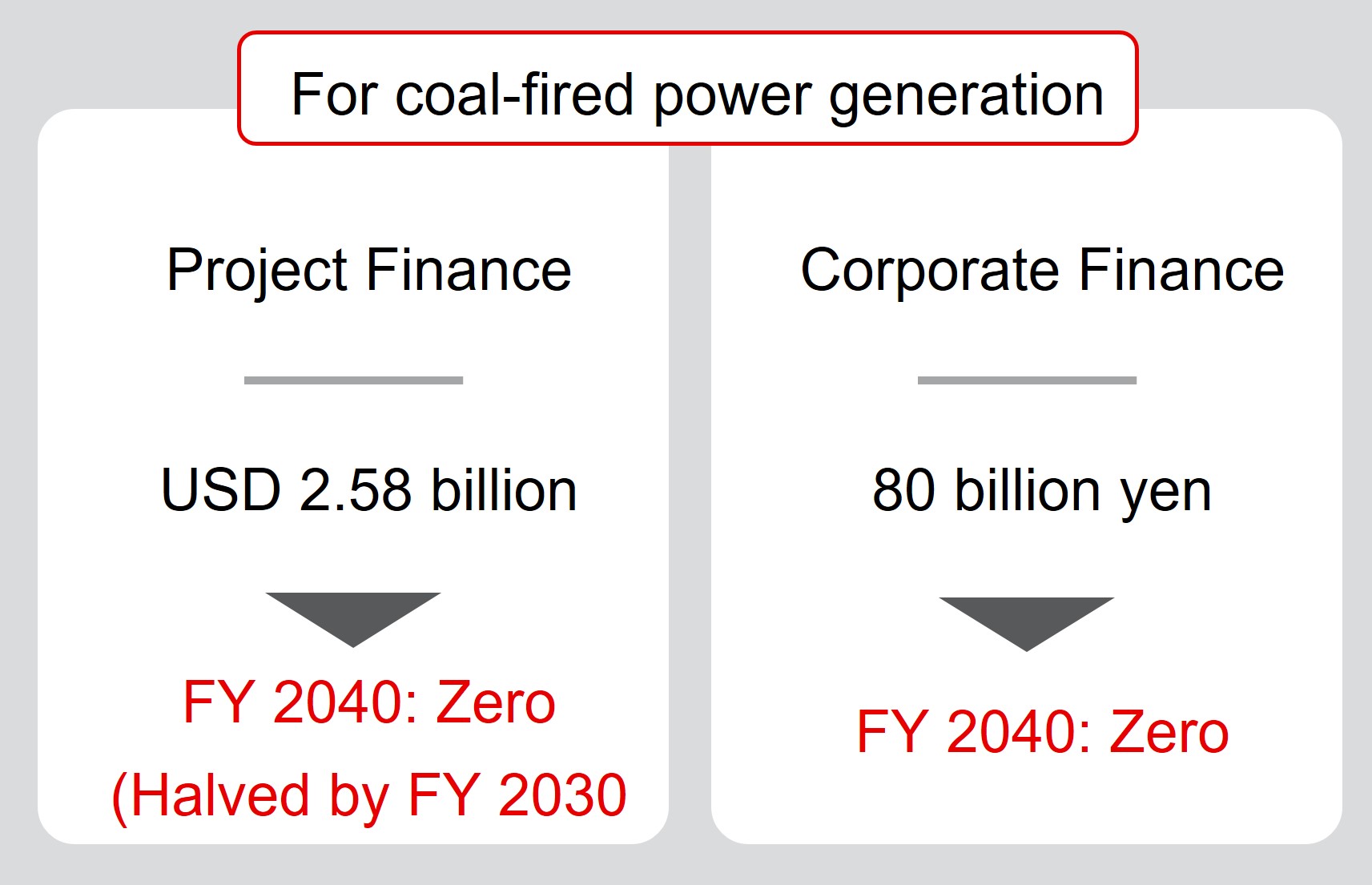

Corporate finance targets for coal-fired power

- Projects that contribute to the transition toward a decarbonized society are excluded following the MUFG Environmental and Social Policy Framework.

■ Oil and gas sector

| Envisioned Business Opportunities | Risk Management |

|---|---|

● Transition to decarbonization business (short, medium, long): M&A and capital investment for new entry and/or expansion into renewable energy generation, bio/synthetic fuel business, etc., and for conversion from gasoline stations to EV and hydrogen station businesses, etc.

● Investment and supply chain development for decarbonized fuels, etc. (short, medium, long): Funding for R&D, demonstration projects, and practical application of hydrogen, ammonia, synthetic fuels, etc., and fund raising associated with supply chain development

● Investment in decarbonization of fossil fuel businesses (short, medium, long): Investment in upgrading existing equipment, electrification, adoption of CCUS, etc. |

● Reduction of GHGs from financed portfolio Interim target setting, performance management ● Management of transition risks Understanding and confirming transition strategies through engagement ● Reduction of environmental and social risks based on ES policy Confirmation of environmental and social consideration for oil sands, Arctic development, shale oil and gas, and pipelines |

Calculation methodology of absolute emissions in the oil and gas sector

| Target scope | Value chain: Upstream production businesses (including integrated businesses heavily involved in upstream businesses) Emission scope: Scope 1, 2, 3 |

|---|---|

| Asset scope | Loan amounts (including undrawn-committed amounts)(note) (note) More than 85% of the exposure is included in the calculation. |

Target metric |

Absolute GHG emissions (MtCO2e) |

| Data source | Information disclosed by each customer, CDP, Bloomberg, etc. |

(Target Scope)

According to PACTA, upstream businesses of fossil fuel sectors are important as they have significant impact on other segments down the value chain. Therefore, MUFG focuses on the upstream of the value chain, which have the largest environmental impact. The emission scope which we look into covers not only Scope 1 and Scope 2 but also Scope 3, from which the majority of GHG emissions from this sector is generated.

(Target metric)

We have chosen to use absolute GHG emissions as the target metric to directly capture fossil fuel burns (Scope 3) which are the main cause of GHG emissions.

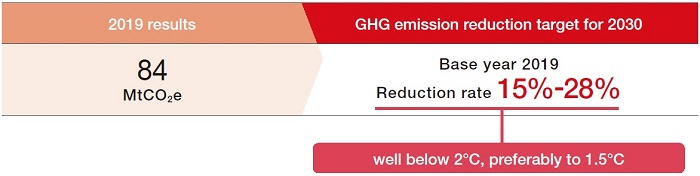

Interim target setting

The interim target for 2030 is 15%-28% reduction from 2019.

We will achieve 15% reduction by engaging with our customers and supporting their efforts in reducing GHG emissions. 15% reduction is a level well below the IEA 2˚C scenario in 2030.

We aim for 28% reduction which is consistent with the IEA 1.5˚C scenario in 2030. However, to achieve this it is essential for both the oil & gas sector (supply-side) and the industries (demand-side) to simultaneously accelerate decarbonization. Therefore, we intend to achieve 28% reduction by making contribution to the world to further advance toward decarbonization.

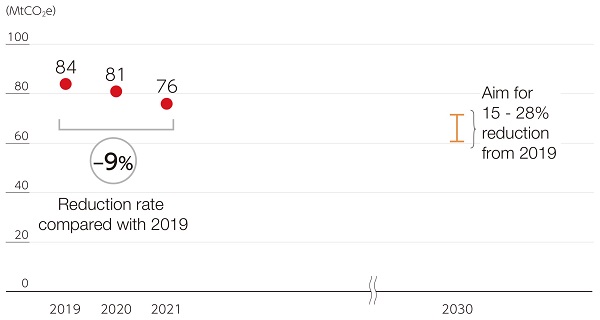

Results over time

| Target for implementation | Outline of initiatives |

|---|---|

| Initiatives with Japanese companies | The MUFG group works as a unified whole to support customers in the oil and gas sectors in formulating strategies for companies' transitions, including the introduction of hydrogen, ammonia, biofuels, and synthetic fuels. While providing customers with analyses of the impacts of ESG response on corporate value and analyses of trends in information disclosure, we provide support for individual projects by working to grasp trends and the business environment in the sector through discussions with customers and by working towards the decarbonization of refinery complexes overall through participation in discussions with local governments and councils. |

MUFG supports individual projects aimed at achieving transitions, based on customer engagement deepened through the MUFG Transition White Paper issued in October 2022. MUFG served as an arranger to undertake a major gas company's first transition loan project using the syndication method. |

|

| Company D (EMEA) | MUFG has proactively been engaging with a leading O&G firm around its transition strategy and discussing the role of ESG in accessing financing in the future. This has led to multiple discussions and engagement with a number of stakeholders – such as senior members of finance and sustainability teams - around the Company. Through these efforts, MUFG is providing long-term support to the client to help our client realize carbon neutrality. |

| Company E (APAC) | To support clean energy transition in Indonesia, MUFG has established engagements with the client on multiple fronts. MUFG has supported the client promote their energy transition through providing financing towards renewable energy projects, participating in a syndicated loan for solar energy projects and acting as a Joint Bookrunner for a green bond issued for geothermal energy projects. |

■ Real estate sector

The real estate sector is a carbon intensive sector that accounts for 8% of global GHG emissions, and 75% of the emissions in this sector come from building utilization. Therefore, the key to decarbonizing the real estate sector is to improve building energy efficiency, install renewable energy equipment, promote electrification, and improve the emission factor for electricity used in buildings.

In particular, the real estate sector has strong regional characteristics influenced by the location of properties including climate conditions, as well as the degree of electrification and energy mix in each country. MUFG‘s portfolio is focused largely on Japan, thus it is important for MUFG to support the initiatives in the Japanese real estate sector and the policies of the Japanese government.

| Envisioned Business Opportunities | Risk Management |

|---|---|

● Renovation of existing buildings (short, medium, long): Demand for loans to improve thermal insulation performance through renovation of existing buildings

● Construction of decarbonized buildings (short, medium, long): Demand for loans for new ZEH(note) housing construction, etc.

● Decarbonized urban development (short, medium, long): Investment in decarbonized urban development that integrates housing, buildings, and transportation systems

● Technology and supply chain development for decarbonized building materials, etc. (medium, long): Fund raising associated with the construction of supply chains for decarbonized concrete, etc. |

● Reduction of GHGs from financed portfolio Interim target setting, performance management ● Management of transition risks Understanding and confirming transition strategies through engagement |

- Net Zero Energy House. Housing equipped with substantial outer insulation and high-efficiency energy-saving equipment, consuming net-zero or negative annual primary energy consumption due to renewable energy, etc.

Calculation methodology for emissions intensity in the real estate sector

| Target scope | Value Chain: Building utilisation Emission Scope: Scope 1, 2 and 3-13(note) of developers, REITs and SPVs, Scope 1 and 2 of mortgage borrowers (note) Emissions from assets leased to others |

|---|---|

| Asset scope | Loan amounts (including undrawn-committed amounts)(note) (note) More than 70% of the exposure is included in the calculation. (For residential real estates, the most recent loan amounts are used due to date availability) |

Target metric |

Emission intensity (kgCO2e/㎡) |

| Data source | Information disclosed by each customer and statistics from various external sources |

(Target scope)

Following NZBA and SBTi, we scope in the emissions from building utilization, which account for almost 80% of the emissions from this sector. For commercial real estate, these are emissions from the use (including leasing) of properties (i.e. Scope 1, 2, and 3-13) owned by corporate customers such as real estate developers, REITs, SPVs(note), etc. For residential real estate, these are emissions from the use of properties (i.e. Scope 1 and 2) that are collateralized to secure mortgage loans (including apartment loans).

- Special purpose vehicles for real estate securitization

(Target metric)

Real estate plays an indispensable role in our daily lives and economic activities. Since it is necessary to support the increase in demand associated with economic growth whilst promoting decarbonization, we chose emission intensity (kgCO2e/㎡) as the target metric for both commercial and residential real estate.

Interim target setting

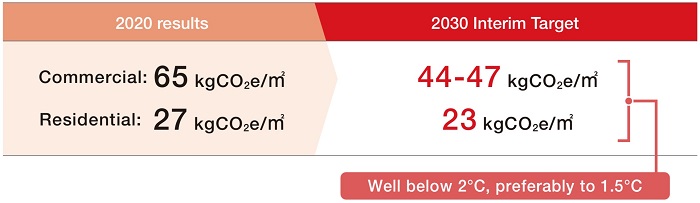

<Commercial Real Estate>

The 2030 interim target (emission intensity) is 44-47kgCO2e/㎡.

We will achieve 47kgCO2e/㎡ by engaging with our clients to meet their own emissions targets. 47kgCO2e/㎡ is well below 2°C level of the CRREM(note) scenario for 2030. In addition, by further contribution to the decarbonization of the emissions from tenancy as well as the power sector, we aim to achieve 44kgCO2e/㎡ to reach 1.5°C level of the CRREM scenario for 2030.

- An initiative that calculates and provides scenario benchmark values for 2°C and 1.5°C by building types and regions covering 28 countries across Europe, Americas, and APAC including Japan.

<Residential Real Estate>

The 2030 interim target (emission intensity) is 23kgCO2e/㎡.

In addition to providing support for energy efficiency and renewable energy solutions for existing collateralized buildings whilst pursuing decarbonization of the power sector, we expect to increase the volume of our ZEH transactions in line with predicted growth of ZEH in the market. Through these measures, we aim to achieve 23kgCO2e/㎡ to reach 1.5 level of CRREM scenario for 2030.

| Target for implementation | Outline of initiatives |

|---|---|

| Hoshino Resorts REIT, Inc. | This corporation has established its own green finance policy framework through which it addresses environmental conservation, climate change, and energy usage. MUFG provided support for green loans to fund green projects including Hoshinoya Karuizawa, which reduces its environmental load through the use of hydroelectric power generation and geothermal heat. |

| MUFG Private REIT, Inc. | This corporation is strengthening its initiatives aimed at real estate sustainability as a form of Responsible Property Investing, and engages in actions including participation in GRESB(note) evaluation. MUFG provided support to the corporation through the first Sustainability Lined Loan for a private REIT. The loan was set using a high 4-star evaluation in the GRESB rating as a sustainability performance target (SPT). (note) An annual benchmark evaluation that measures environmental, social, and governance (ESG) consideration by real estate companies and funds. Also, the name of the organization that operates the evaluation. |

| MITSUBISHI ESTATE CO., LTD. | MUFG is backing up the carbon neutrality initiatives of this company, which has announced its "Net Zero Declaration for 2050." MUFG supported the issuance of Sustainability Linked Bonds through securities with SPTs of "achievement of 100% electric power derived from renewable energy sources in FY2025" and "achievement of 70% or greater reduction in total Scope 1 and 2 GHG emissions and 50% or greater reduction in Scope 3 emissions in FY2030 (compared with FY2019 levels)”. The Bank supported a Sustainability Linked Loan with the SPT of "achievement of 100% electric power derived from renewable energy sources in FY2025." The SPTs in Mitsubishi Estate's Sustainability Linked Finance Framework (as of March 2023) are in line with the Net-Zero Standard announced by SBTi in October 2021. |

| Tokyu Fudosan Holdings Corporation | Tokyu Fudosan Holdings Corporation, the Trust Bank, and the Bank have formed the first green finance-certified money trust for individuals in Japan. The green finance-certified money trust for individuals is the first such initiative in Japan (note). The loan claims executed by the Bank for the company are transferred to the Trust Bank, which then sells trust beneficiary rights from the money trust managed by the Trust Bank using loan claims to individual customers. The use of funds from the loan claims is limited to construction funds for condominium brands that proactively address the environment. Through this product, we are working to meet the financial management needs of individual customers as well as to solve ESG issues. (note) According to research by the Mitsubishi UFJ Trust and Banking Corporation. As of February 8, 2023. |

| Company F (APAC) | MUFG took a lead in advising the client, one of the leading property developers in Hong Kong, to incorporate sustainability-linked loan format into the Facility. MUFG was mandated as one of the three sustainability advisors and led one of the largest sustainability-linked loan deals for the real estate sector in Hong Kong. |

■ Steel sector

The steel sector is a carbon intensive sector that accounts for 7% of global GHG emissions, and 77% of the emissions in this sector come from steel production. Decarbonization of the steel sector will be driven by decrease in blast furnace production and increase in scrap reuse, the development of low-carbon manufacturing technologies, and the implementation of CCUS to collect non-reducible carbon.

As the Japanese steel sector is expected to play a central role in responding to the increasing demand for high-quality steel, it will be necessary to confront the long-term challenge of developing technologies such as hydrogen reduction in blast furnaces, 100% hydrogen direct reduction processes, and large electric furnaces. With about 90% of MUFG’s steel portfolio being comprised of major Japanese companies, we are committed to supporting them with these efforts toward decarbonization.

| Envisioned Business Opportunities | Risk Management |

|---|---|

● Development of decarbonized steelmaking technology (short, medium, long): Fund raising associated with R&D, demonstration projects, and practical application of hydrogen utilization in blast furnaces, hydrogen direct reduction, utilization of electric furnaces, etc.

● Procurement of decarbonized fuels, etc. and supply chain development (short, medium, long): Fund raising associated with the development of supply chains for hydrogen, CCUS, etc.

● Business diversification (short, medium, long): M&A and capital investment for new entry and expansion |

● Reduction of GHGs from financed portfolio Interim target setting, performance management ● Management of transition risks Understanding and confirming transition strategies through engagement |

Calculation methodology of absolute emissions in the steel sector

| Target scope | Value chain: Steel production Emission Scope: Scope 1 and 2 of steel manufacturers |

|---|---|

| Asset scope | Loan amounts (including undrawn-committed amounts)(note) (note) Around 90% of the exposure is included in the calculation |

Target metric |

Absolute GHG emissions (MtCO2e) |

| Data source | Information disclosed by each customer, CDP, Bloomberg, etc. |

(Target Scope)

Following SBTi and PACTA, we scope in the emissions from steel production, which accounts for almost 80% of the emissions from this sector (i.e. Scope 1 and 2 of steel manufacturers).

(Measurement Metrics)

We have chosen to use absolute GHG emissions as the target metric as this is the metric used by the majority of the customers in our portfolio, thereby enabling us to directly follow the progress of customers in reducing their GHG emissions. We used 2019 as the baseline year for this sector, as emissions fell significantly in 2020 as a result of cutbacks in steel production due to the significant impact of COVID-19.

Interim target setting

| Target for implementation | Outline of initiatives |

|---|---|

| Initiatives toward Japanese companies | MUFG engages in regular exchanges of ideas at the management level with customers in the steel sector to discuss characteristics of the Japanese manufacturing and steel-making industries, issues in innovative technology development, and trends in the external environment. We work to understand the circumstances of customers from more diverse perspectives through study tours of steel mills and peripheral technologies. Based on this, we conduct ongoing dialogue to support customers in achieving transitions. |

| Company G (APAC) | MUFG supports the company in its decarbonization journey across various business verticals. MUFG conducted a series of engagement sessions and assisted the power and steel business to identify Eligible Green Projects to be financed using Sustainable Finance debt instruments as part of the company’s aspiration towards net-zero by 2045. |

■ Shipping sector

The shipping sector is a carbon intensive sector that accounts for 2% of global GHG emissions, and 98% of emissions in this sector come from shipping operations (i.e. fuel consumption). Therefore, the key to decarbonization is to switch to LNG fuel and implement measures to save energy and improve operational efficiency during transition period, and ultimately introduce zero-emission fuel vessels (i.e. hydrogen/ammonia/methanol, biofuels, etc.).

Whilst available type of fuel is limited by the type and size of vessels, each vessel is used for specific purposes, and it is not easy to substitute one vessel type with another. Therefore, it is important to consider operational efficiency and smooth decarbonization pathways for each type of vessel, and new fuel development and early implementation of technological innovation is the shipping sector’s next challenge.

MUFG joined the Poseidon Principles in March 2021. Under this framework, MUFG has been disclosing its ship finance portfolio climate alignment starting from 2022 using the data of 2021.

<Poseidon Principles>

A framework for calculating, assessing and disclosing the climate alignment score of ship finance portfolios in order to achieve the International Maritime Organization’s (IMO) GHG emission reduction targets. The degree to which the annual average carbon intensity for each vessel in the financial institutions’ portfolio deviates from its respective trajectory based on the scenarios referenced by the Poseidon Principles will be assessed using the Vessel Climate Alignment (VCA) and the Portfolio Climate Alignment (PCA). |

| Envisioned Business Opportunities | Risk Management |

|---|---|

● Support for decarbonization in shipping (short, medium, long): Fund raising associated with R&D, demonstration projects, and practical application of energy conservation in existing vessels, streamlining of operations, and zero-emission fuel-ships (hydrogen, ammonia, methanol, bio-fuels, etc.)

● Investment in shipping that contributes to decarbonization (short, medium, long): Investment in shipping that supports decarbonization of CO2 transport vessels engaged in the CCS/CCUS business, vessels related to the offshore wind power business, etc. |

● Reduction of GHGs from financed portfolio Setting of PCA targets and confirmation of results ● Management of transition risks Understanding and confirming transition strategies of shipping companies through engagement |

Assumptions for PCA calculation in the shipping sector

| Target scope | Value chain: Operation (fuel consumption) Emission Scope: Scope 1 (TTW(note)) of shipping operators (note) Tank to Wake: CO2 emissions from the ship’s fuel tank to the exhaust |

|---|---|

| Asset scope | Ship finance tied to vessels under purview of IMO(note) (note) Emissions data reporting rate (as of December 2021): 71.4% |

Target metric |

Portfolio Climate Alignment (PCA) |

| Data source | Information disclosed by each customer (IMO Data Collection System (IMO DCS) data) |

(Target Scope)

In line with the guidance from Poseidon Principles, we scope in the emissions from operation, which accounts for more than 90% of emissions from this sector (i.e. Scope 1 of shipping operators).

Measurement Metrics

Following the Poseidon Principles, we are utilizing emission intensity-based PCA as our target metric.

PCA score for 2021 was +0.6%, which means a deviation of +0.6% from the Poseidon Principles reference scenario (i.e. IMO scenario aiming for 50% GHG reduction by 2050 from 2008(note)).

- IMO target at the time of PCA calculation in 2021

Interim target setting

We have set the 2030 interim target (PCA) as 0% or less. This means that the intensity of vessels financed by MUFG, at the portfolio level, will be consistent with the IMO scenario which aims to reduce the total GHG emissions by 50% from 2008 baseline (by 2050).

MUFG aims to achieve this goal by proactively supporting decarbonizing initiatives promoted in the shipping sector, such as implementing measures to save energy and improve operational efficiency, promoting the use of biofuels, developing hydrogen and ammonia vessels, and switching to LNG fuel during transition period.

In July 2023, IMO adopted a revision to its scenario that aims for net-zero total GHG emissions by or around 2050, compared to 2008 level. In response to this, the Poseidon Principles have already announced development of a framework consistent with the revised IMO scenario. MUFG will update its scenarios in line with action by the Poseidon Principles.

| Content of Initiatives | Outline of initiatives |

|---|---|

| Engagement | In December 2022, MUFG released a PCA score based on the Poseidon Principles. The PCA shows the degree to which CO2 emissions based on fuel consumption from financed ships deviate from the GHGs reduction scenario set by the Poseidon Principles. Based on the scores, MUFG discussed with customers on initiatives for decarbonization. We will continue using knowledge gained from Poseidon Principles initiatives in discussions with customers and support the decarbonization in financial terms. |

| Financing support for existing technologies | MUFG provides financing for vessels that effectively reduce GHGs to achieve decarbonization in the shipping sector. As an example, LPG and LNG, typical marine fuels during the transition period, reduce sulfur oxides (SOx) by 95% to 100% and CO2 by 20% to 30% or more compared to conventional marine fuels. Through financing for LPG dual-fuel large gas carriers, LNG dual-fuel LNG carriers, car carrier ships, and container carrier ships, MUFG supports decarbonization in the shipping sector. |

| Financing support for new technologies | In the area of zero-emission-fuel ships, advancements are being made in the development of engines, construction of supply chain networks for zero-emission fuels, and expansion of bunkering facilities. Recognizing that the proliferation of these ships holds a key to decarbonization, MUFG is studying financing for ammonia dual-fuel ships and methanol dual-fuel ships. We will continue researching industry trends and holding discussions with customers as we study support for zero-emission-fuel ships, CO2 transport ships, and other forms of shipping that are expected to require the development of new technologies. |